A single traffic citation can trigger an insurance premium impact that lasts for years. Insurance companies use your driving record as a primary factor when calculating your rates, and violations signal increased risk to insurers.

At floridanewdriver.com, we’ve seen firsthand how a ticket can catch drivers off guard with rate hikes of 20% to 50% or more. The good news is that understanding how citations affect your premiums-and knowing what steps to take afterward-can help you minimize the damage.

How Insurance Companies Track and Price Your Violations

State Point Systems Shape Your Risk Profile

State point systems assign specific points to traffic violations, and these points form the foundation of how insurers assess risk. Arizona adds 3 points for speeding, while Nevada assigns 1�5 points depending on the violation’s severity. These points typically stay on your driving record for one year in Nevada, but insurers look back much further than that timeframe. Driving history is a key factor insurers use to calculate your rates, which means a violation from three years ago can still affect your premium today.

Multiple Violations Compound Your Rate Increases

When you accumulate multiple violations within a short period, insurers view you as a significantly higher risk, and your rate increase compounds accordingly. A driver who received two speeding tickets in 2021 saw their monthly premium jump from $65 to $200-a 208% spike. Four years later, even with a clean driving record since those tickets, their quotes remained around $130 for basic coverage, demonstrating how long violations linger in the pricing calculation.

Insurers Monitor Violations for Years

Insurers typically monitor violations for three to five years, though serious offenses like DUI can stay on your record much longer. California DUI violations, for example, can affect your rates for up to 10 years. Most insurers reassess your risk at every policy renewal, not just when you first purchase coverage, which means a ticket can trigger a rate increase even if you had a clean record when you signed up. Recency matters significantly-newer tickets weigh more heavily in underwriting models than older ones.

Timing and Carrier Differences Matter

After three years without additional violations, some insurers begin removing the impact from their pricing algorithms, though this varies widely by carrier. Shopping around matters because different insurers weight violations differently in their underwriting. One carrier might impose a 30% increase while another charges 50% for the identical violation and driving history. The sooner you compare quotes from multiple insurers after receiving a citation, the better your chances of finding one that treats your violation less severely than your current provider.

Understanding how insurers track and price your violations sets the stage for exploring which specific violations cause the most dramatic rate hikes-and why some citations cost far more than others.

Which Violations Cost You the Most

Hit-and-Run and DUI Violations Carry the Harshest Penalties

Hit-and-run and DUI violations trigger the most severe insurance penalties. A DUI typically adds about $2,214 per year to your baseline costs. Reckless driving ranks close behind, and racing violations push rates up by approximately 93%. The Zebra’s analysis of millions of insurance quotes across U.S. zip codes using consistent driver profiles confirms these figures reflect real pricing patterns, not theoretical estimates.

Speeding and Common Moving Violations Add Substantial Costs

Speeding violations fall into a lower tier than DUI or reckless driving, yet they still impose significant financial consequences.

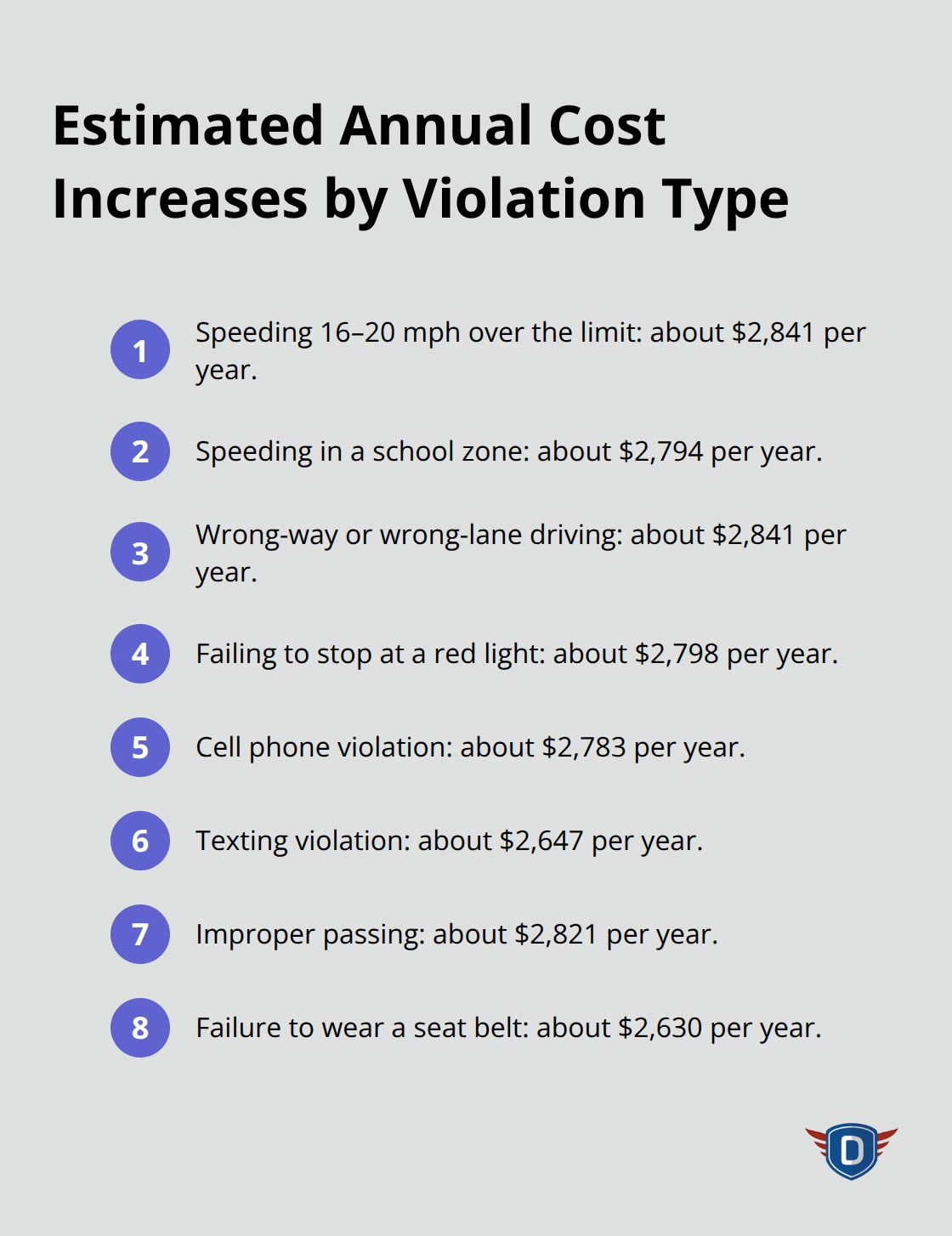

Speeding 16�20 mph over the limit increases your annual premium by roughly $2,841, while speeding in a school zone costs approximately $2,794 per year. Wrong-way or wrong-lane driving violations add about $2,841 annually, and failing to stop at a red light runs approximately $2,798. Cell phone and texting violations contribute around $2,783 and $2,647 respectively, while improper passing adds roughly $2,821. Even failure to wear a seat belt carries a penalty of approximately $2,630 per year.

Geographic Location Dramatically Alters Your Rate Increase

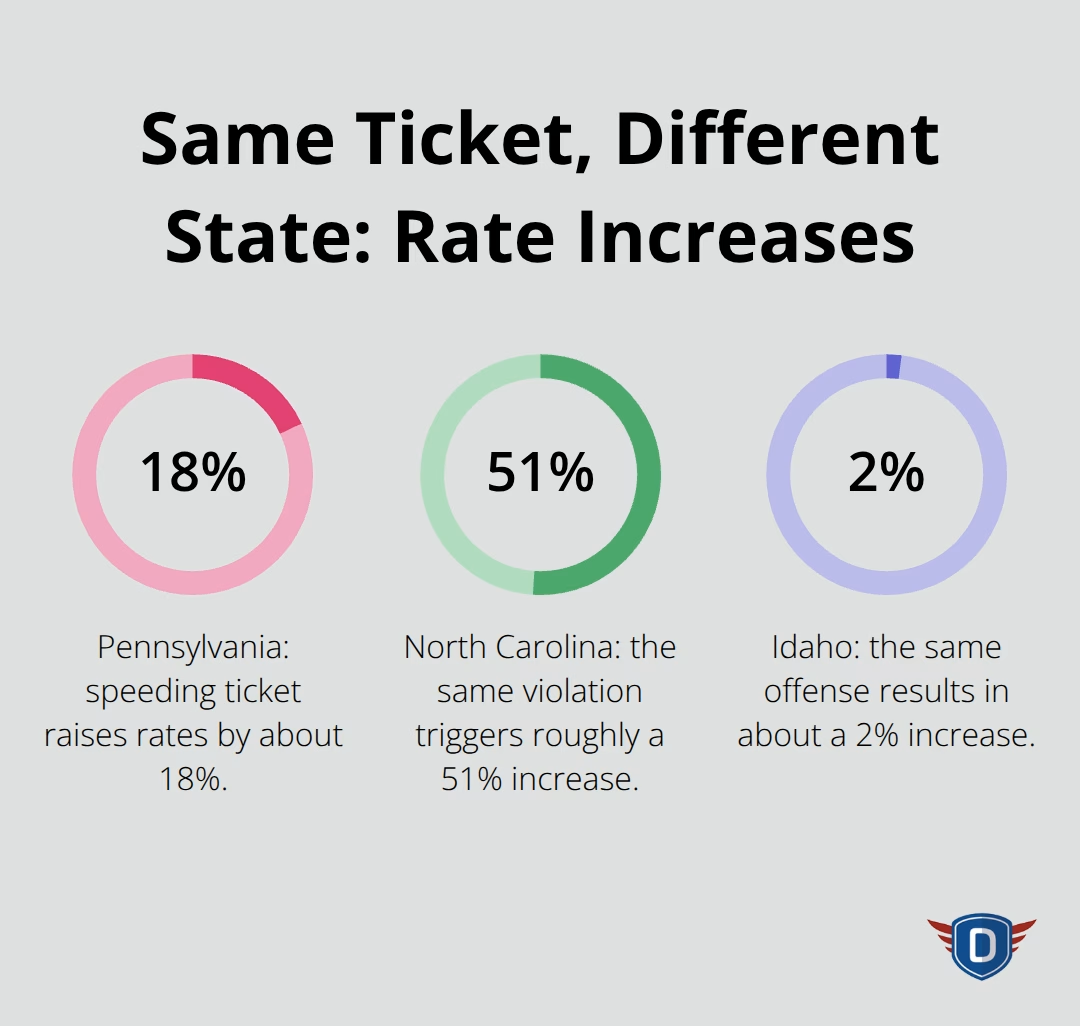

Geographic location dramatically alters insurance rate increases for identical violations. In Pennsylvania, a speeding ticket increases rates by only about 18%, but the same violation in North Carolina triggers a roughly 51% increase. California DUI violations can skyrocket rates by up to 310%-nearly $5,000 annually-while Idaho experiences only about a 2% increase for the same offense.

These disparities reflect different state regulations, insurer practices, and risk assessment models unique to each region, meaning your location matters as much as the violation itself.

Multiple Violations Within Three Years Compound Financial Damage

Accumulating multiple violations within a short period transforms a manageable rate increase into a long-term financial burden. One driver received two speeding tickets in 2021 and watched their monthly premium jump from $65 to $200-a 208% spike. Four years later, with a clean driving record since those tickets, their quotes remained elevated around $130 monthly, demonstrating how violations persist in pricing calculations well after you’ve paid the fine. This compounding effect makes the first few years after multiple citations especially costly.

Different Insurers Weight Identical Violations Completely Differently

Shopping around immediately after a citation becomes essential because carriers assess risk using different underwriting models. One insurer might impose a 30% penalty while another charges 50% for the identical infraction and driving history, making the difference between manageable costs and excessive premiums substantial. The sooner you compare quotes from multiple carriers after receiving a citation, the better your chances of finding one that treats your violation less severely than your current provider.

Understanding which violations carry the highest costs sets the stage for exploring concrete strategies to reduce your premiums after a citation-and how taking action quickly can minimize long-term financial damage.

Reduce Your Rates After a Citation

Traffic School Courses Keep Violations Off Your Record

Traffic school courses and defensive driving programs offer concrete pathways to lower your insurance costs after a citation. Many states allow drivers to complete an approved traffic safety course to keep violations off their driving record entirely, which prevents insurers from seeing the citation when they pull your history. The cost of taking a course typically ranges from $30 to $150 depending on your state and provider, but this investment pays for itself quickly when you consider the potential impact on your premium. Insurance providers offer discounts of 5% to 20% for drivers who complete approved defensive driving courses, which can result in substantial savings over time.

However, not all violations qualify for traffic school removal, and not all insurers recognize every course. Contact your current carrier before enrolling to confirm they’ll honor the completion certificate and reduce or waive the rate increase.

Shop Around Immediately After Your Citation

Shopping around for new insurance quotes immediately after receiving a citation is far more valuable than most drivers realize, because different insurers apply wildly different penalties for identical violations. One carrier might impose only a 30% increase while another charges 50% for the same speeding ticket and driving history, creating a potential annual savings of hundreds or even thousands of dollars. The sooner you compare quotes from multiple insurers, the better your chances of finding a carrier that treats your violation less severely than your current provider.

Some insurers also offer usage-based or telematics programs that reward safe driving behavior, potentially offsetting post-ticket increases by monitoring your actual driving habits rather than relying solely on your violation history.

Multiple Violations Require Urgent Action

If you’ve accumulated multiple violations within three years, your rate impact compounds, making the search for a new carrier even more critical. Some insurers specialize in drivers with violations while others penalize them harshly, so the difference between carriers can be substantial. After you’ve completed a traffic course or after three years have passed since your last violation, requote with different insurers because some carriers reset their risk assessment at that point, leading to substantially lower rates than you’d receive if you stayed with your current provider.

Final Thoughts

Traffic citations impose a lasting financial burden that extends far beyond the ticket fine itself. Your insurance premium impact from a single violation persists for three to five years, with serious offenses like DUI affecting your rates for a decade or longer. The data shows that a speeding ticket can cost you thousands in elevated premiums, while multiple violations within a short timeframe compound the damage exponentially.

After receiving a citation, complete an approved traffic safety course if your state allows it, then shop around for new quotes from multiple insurers within days of the violation. Different carriers weight identical infractions completely differently, so switching providers could mean hundreds or thousands in annual savings. Some insurers offer usage-based programs that reward safe driving habits, potentially offsetting the impact of past violations through your actual driving behavior.

Safe driving over the next three to five years remains your most powerful tool for recovery. Once you maintain a clean record for that period, requote with different insurers because some carriers reset their risk assessment at that point, leading to substantially lower rates. If you’re facing a citation or working to improve your driving record, floridanewdriver.com offers Florida-approved traffic school courses designed to help you reduce points, meet court requirements, and qualify for insurance discounts.